Sharing our insights into the biggest sustainability challenges facing our built environment. We begin the series by looking at cooling, the massive problem no one is talking about.

The Problem

TL;DR fixing the issue of energy efficiency and refrigerants in the hardware that keeps us cool could avoid 460 GtCO2e over the next four decades (IEA). We must tackle three concurrent problems 1) Energy efficiency of air conditioners 2) the energy mix and the demand on the grid to power them 3) the refrigerants inside them.

As the world warms humanity will switch it to relying on cooling from comfort to requiring to survive. The search for the term “Wet bulb temperature” spiked on Google last summer as humidity, temperature (and deaths) rose across the globe. It’s only going to get worse: “30% of the world’s population is exposed to a deadly combination of heat and humidity for at least 20 days each year, that percentage will increase to nearly half by 2100, even with the most drastic reductions in greenhouse-gas emissions” (Nature Climate). In a 1.5 ◦C world, 13.8% of the world population will be exposed to severe heat waves at least once every 5 years. This fraction becomes nearly 3x larger (36.9%) under 2 ◦C warming, i.e. a difference of ~ 1.7 billion people. Limiting global warming to 1.5 C will also result in around 420 million fewer people being frequently exposed to extreme heat waves, and ∼65 million to exceptional heat waves (IOP).

Growing Demand

The IEA predicts that global shipments of air conditioning units will grow by 3x by 2050 to 5.6 billion units with 2.5 billion of those shipping into China and India. India alone will go from 50 million units to 1.1 billion. If all of those units continue to use the current cooling architecture our current energy grid will be unable to power them and their planetary impact will be in the hundreds of gigatonnes over the decades to come.

Energy needs and mix

For those of us in countries where air conditioning is already widespread, keeping us cool consumes up to half of the energy needs of the average American home.

To put the scale of this in context, in 2016 the global electricity demand for cooling equaled 2,000 TWh the equivalent total electricity consumed in Japan and India that year (IEA). That is expected to triple to 6,000 TWh by 2050. Our current global grid infrastructure is not set up to deal with this increase in demand.

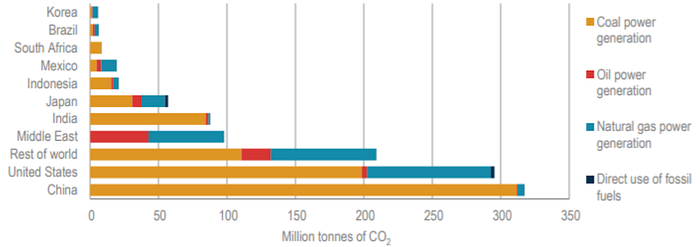

Unfortunately cooling demand also correlates highly with peak energy demand and is therefore powered by fossil fuel sources, exacerbating their impact. In some countries in the Middle East the cooling demand can be as high as 50 % or more during peak load (IEA, 2018).

Energy Efficiency

The global HVAC market is highly consolidated with four players dominating 67% of sales: Daikin, Trane, Carrier and JCI York followed by a long tail of regional players.

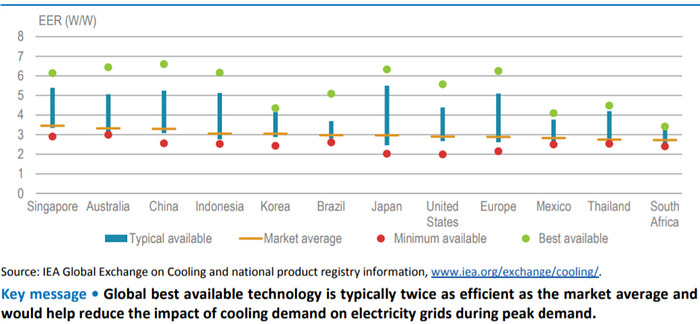

Unfortunately the architecture of an AC unit has not changed much since Willis Carrier invented it in 1902 to solve the humidity problem in a paper pulp plant (highly recommend this podcast by the BBC on the history of AC). What has improved over time is the energy efficiency of best-in-class AC units. What the average residential or commercial consumer buys or has installed, however, is closer to the worse-in class. So the current existing stock of over 2 billion units is less than half as efficient as the best available technology.

The irony of this, is that the lower income family who buys a new AC unit in India or Central America will likely make the choice based on purchase price and therefore acquire a low efficiency unit which will then be price-prohibitive to run given electricity required to power it.

Aware of the impact it will have on its citizens and its grid, the Indian government and RMI recently sponsored the Global Cooling Prize, a challenge program that sought to identify solutions that were at least 5 times less impactful than the status quo with “a 60 percent reduction from baseline, and a 30 percent reduction from typical high performing units available in the market.”

Refrigerants

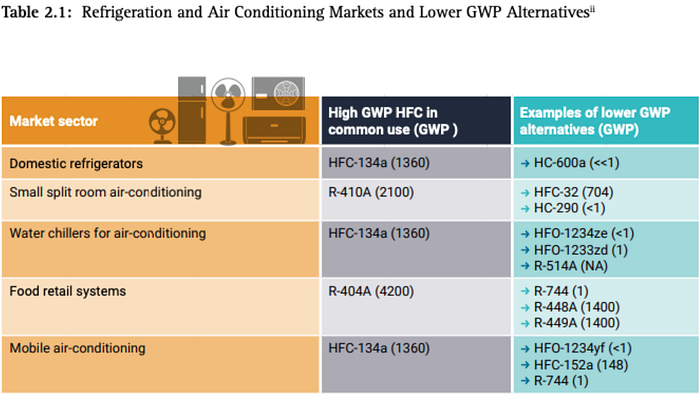

The final challenge with cooling is the chemicals used to power current architectures. HFCs or Hydrofluorocarbons are the most common refrigerants. These are, unfortunately, very bad for our planet with up to 4,000 times the warming impact of CO2. Most of the impact of refrigerants occurs at the end of life of cooling units when they leak into the atmosphere. Project Drawdown states that “over thirty years, containing 87 percent of refrigerants likely to be released could avoid emissions equivalent to 89.7 gigatonnes of carbon dioxide.”

Luckily there is a political push (and will) to impact HFCs with the Kigali Amendment to the Montreal Protocol. The goal is to achieve over 80% reduction in HFC consumption by 2047. The impact of the amendment will avoid up to 0.5 °C increase in global temperature by the end of the century. The United States passed its HFC reduction legislation. Given the number of US-based “club of four” HVAC OEMs this might spur new alternatives being pursued more quickly.

A number of alternative refrigerants are being pursued. Some of them, however, pose other challenges like flammability (Butane) which in some countries limits its ability to be used in systems that feed directly into building air ducts. Below is a list of alternative refrigerants and their Global Warming Potential (GWP) compared to current HFC in use (UNEP, IEA). For context the GWP of CO2 is 1.

Solutions

To therefore address the critical sustainability challenges of cooling we need to solve three core problems:

- Improve the (mandated) energy efficiency of future-installed cooling units while accelerating the replacement rate of existing stock.

- Find ways to balance the energy load feeding this growing stock either by accelerating the transition to cleaner energy or load balancing their charge.

- Quickly switch to refrigerants with lower GWP

Doing all of the above requires a combination of technological innovation, policy and regulation, and acceptance and acceleration by the incumbents alongside risk-taking investments into emerging technologies.

So where to start?

A first stab would be to consider residential versus commercial as the “vector of attack”

Taking the US as the baseline with a high installed stock, there are almost 2x the installed AC units in homes than in buildings… but the GW output is higher for commercial. Secondly, commercial unit owners *must* provide cooling either due to tenant lease contracts or quality controls in industrial facilities. Finally, commercial cooling users need to have cooling while being more highly attuned to its cost and to regulations (like New York LL97) which incentivise them to prioritise higher energy efficiency and lower costs.

Assumptions that cooling is only a “hot climate” issue are dispelled by the data above and empirical evidence that even buildings in London, Copenhagen, Toronto or Auckland require cooling alongside heating, sometimes on a contractual basis with the owner to ensure stable and consistent temperature.

As price and policy signals in commercial markets create stronger incentives to find more efficient and less impactful cooling solutions, the conditions for innovations to take root are more developed. The hope would be that technologies that deploy into the commercial space in the short term would eventually find their ways into people’s homes.

The Investment Opportunity

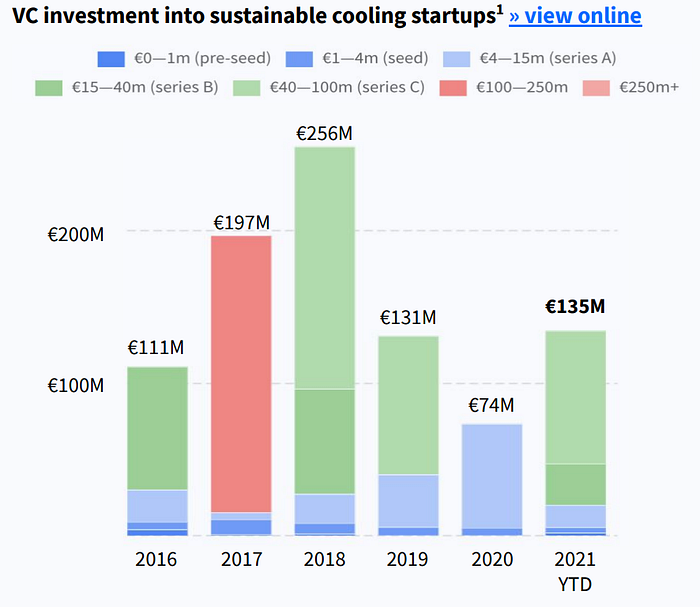

Investment into cooling technologies has been erratic over the past few years.

Initiatives like the Cooling Prize have raised visibility on innovation in the sector — It is particularly interesting to see that the two winners (and most of the finalist) were incumbent OEMs.

It is encouraging to see innovation and focus on cooling as a growing problem set from within the Climate Tech community has grown. As part of our work with Dealroom we mapped the startups and technologies innovating in this critical space.

At 2150 we are actively pursuing investment opportunities in cooling, and our ambition with this post is to help educate others on the magnitude of the problem, and our framework for thinking about potential solutions. Please do reach out if you want to continue learning together or partnering to identify and back scalable cooling technologies.

________

2150 is a venture capital firm investing in technology companies that seek to sustainably reimagine and reshape the urban environment. 2150’s investment thesis focuses on major unsolved problems across what it calls the ‘Urban Stack’, which comprises every element of the built environment, from the way our cities are designed, constructed and powered, to the way people live, work and are cared for. Find out more at www.2150.vc